Reading in English | Read in العربية (Arabic)

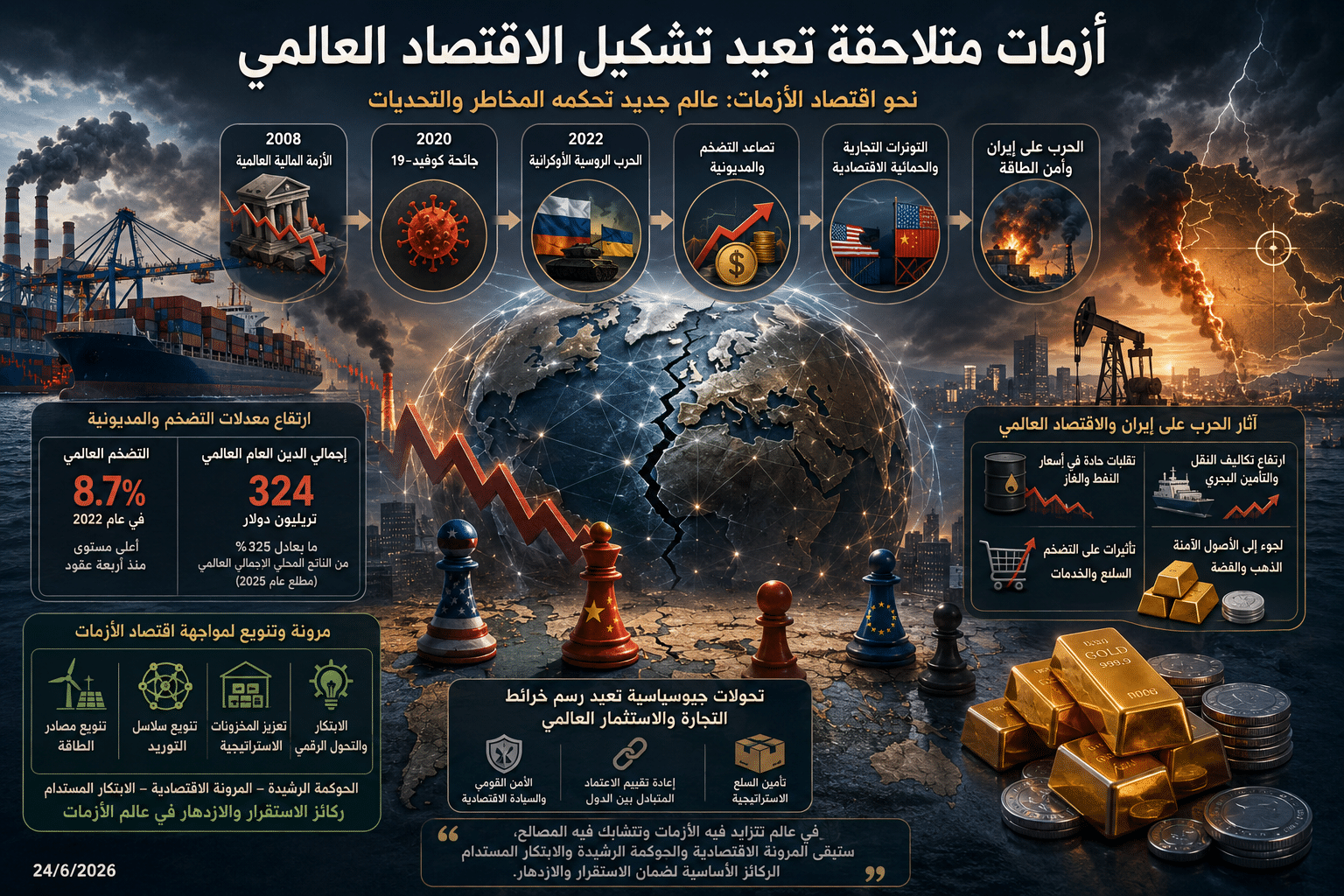

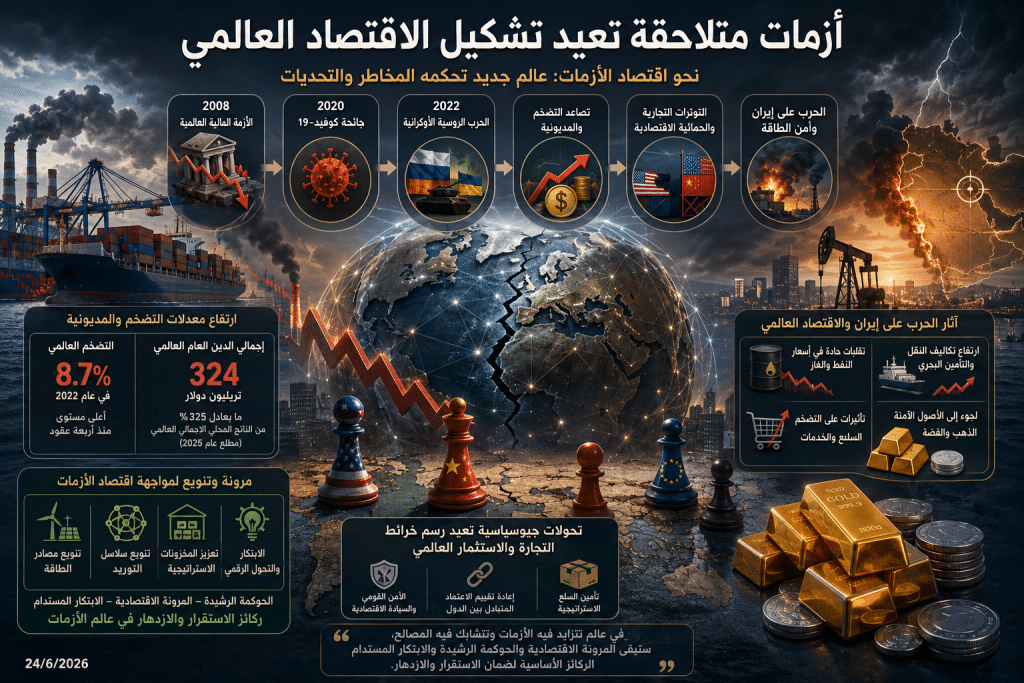

The recent war, along with the rapid international developments and extensive geopolitical and economic ramifications it has caused, has demonstrated that the global economy has entered a new phase known by experts as the “crisis economy.” This shift has emerged after a prolonged period during which economic globalization thrived, characterized by the free flow of goods, capital, and supply chains across borders. This phenomenon marked the period from the early 1990s until the late 2010s.

One of the most significant challenges facing the global economy today is the rising rates of inflation and debt. The signs of this transformation began to appear with the global financial crisis in 2008, which exposed the vulnerabilities of the global economic system and led to a slowdown in international trade. This was followed in 2020 by the COVID-19 pandemic, which exacerbated existing imbalances due to unprecedented disruptions in production and supply chains. Just as the global economies were starting to recover from the pandemic’s effects, the Russia-Ukraine war ignited a severe energy crisis in Europe and a global food crisis, leading to a succession of economic and financial shocks at a rapid pace.

Amid these developments, inflation has emerged as one of the foremost challenges confronting the global economy. The global inflation rate surged to approximately 8.7% in 2022, the highest level recorded in nearly four decades, primarily driven by rising energy and food prices, supply chain disruptions, and increasing transportation and production costs. Consequently, central banks implemented strict monetary policies; for instance, the U.S. Federal Reserve raised interest rates from near-zero levels at the beginning of 2022 to over 5% in less than eighteen months, marking one of the fastest tightening cycles in its modern history.

While these measures helped alleviate inflationary pressures and avoid a severe global recession, they also increased the cost of servicing public debt, intensifying pressure on governments, companies, and individuals. Concurrently, global debt reached record levels, with total global public debt exceeding $324 trillion at the beginning of 2025, equivalent to about 325% of global GDP. This spike in debt has heightened the vulnerability of emerging economies and low-income countries, diminishing their capacity to finance development and investment projects.

The economic policies adopted by former U.S. President Donald Trump played a significant role in accelerating this transformation, as he embraced a protectionist economic approach. This included imposing tariffs, renegotiating trade agreements, and encouraging the relocation of industries back to the United States. As trade tensions heightened, particularly between the U.S. and China, and regional conflicts and economic sanctions intensified, globalization began to lose some of the momentum it had enjoyed for decades.

These changes have led to a reconfiguration of global trade and international investment, prompting a reevaluation of the concept of interdependence among nations. National security and economic sovereignty considerations, as well as securing strategic goods, often take precedence over cost reduction and economic efficiency. As a result, recent geopolitical shifts have created a new economic reality, reshaping the rules of international trade and investment.

The U.S.-Israeli war against Iran has not only redefined the global economy through its direct military impacts but has also deepened the crises confronting the international economic system. This conflict highlighted the extent to which the global economy is intertwined with geopolitical risks, illustrating that any military confrontation in the Gulf or other strategic regions can lead to consequences that transcend regional boundaries, affecting energy, trade, and financial markets worldwide.

Moreover, this war has brought the issue of global energy security back to the forefront, reminiscent of the crises of the 1970s, due to Iran’s strategic position overlooking the Strait of Hormuz, through which about one-fifth of global oil and gas trade passes. Growing concerns about supply disruptions have caused sharp fluctuations in oil and gas prices and increased transportation and maritime insurance costs, directly impacting the prices of goods and services as well as global inflation rates.

In response to these developments, many countries have begun to reassess their economic strategies by diversifying energy sources and supply chains, bolstering strategic reserves, and reducing reliance on sensitive trade corridors to mitigate the impact of potential future geopolitical disruptions. Financially, amid rising uncertainty in global markets, countries and investors have turned to safe-haven assets, particularly gold and silver.

These collective transformations indicate that the global economy is no longer governed by the traditional logic of globalization that prevailed for decades; instead, it has entered a new phase where economic considerations intertwine with security and strategic calculations. In a world marked by increasing conflicts and geopolitical tensions, nations are no longer measured solely by their production volumes or growth rates but also by their resilience to shocks and their ability to secure vital needs while maintaining economic stability.

Consequently, it appears that the “crisis economy” will not be a transient phase but rather a governing framework for the global economy in the foreseeable future. This reality compels countries to reshape their economic policies on more flexible and sustainable foundations, capable of adapting to rapid changes. In a world where crises are escalating and interests are intertwined, economic resilience, sound governance, and sustainable innovation will remain the essential pillars for ensuring stability and prosperity.